{kind=link}

Do we have enough acronyms… and are they the right ones?

Energy loves its acronyms, but it’s not always clear they’re helping. From HEMS to DERMS, this article explores how language meant to simplify can sometimes add to the confusion.

Texas became one of the fastest growing solar and battery markets in the world. Can it keep its speed as OBBB, grid reforms, and demand reshape the energy market?

When people ask what the One Big Beautiful Bill means for clean energy, the easy answer is simple: fewer subsidies, tougher economics, slower deployment. That is true, but it is not the most interesting part of the story. The more interesting question is what happens in a market like Texas, where solar, storage, and flexible load have historically scaled not because policy was perfect, but because the market moved fast.

That was one of the big themes in a recent Texas panel discussion I joined. My view is that OBBB is not best understood as a full stop for clean energy. It is better understood as a stress test. It raises the bar on project quality, timing, procurement, and financing. In weaker markets that can be enough to stall momentum. In Texas, the bigger issue may be different. The real question is whether the state can keep the speed advantage that made it so attractive in the first place.

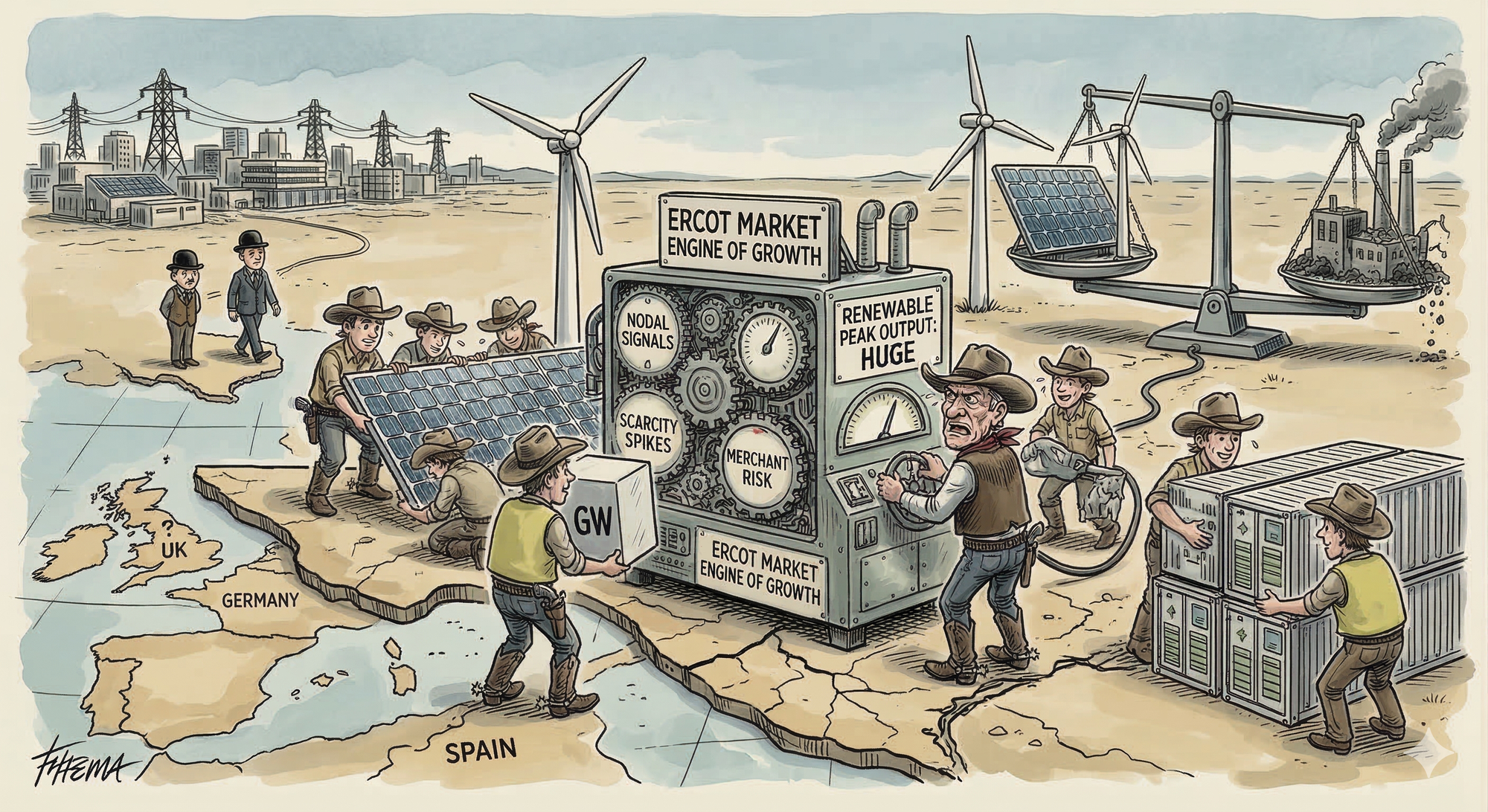

Texas now sits in a remarkable position. The ERCOT grid operates with well over 30 GW of installed solar capacity, a rapidly expanding battery fleet measured in the tens of gigawatts, and more than 40 GW of wind generation¹. At peak moments the system has already seen extremely high combined output from wind and solar, reflecting just how quickly renewable generation has scaled in the state.

The shift is visible in the generation mix as well. Solar generation in ERCOT has recently surpassed coal for the first time, highlighting the speed at which the system has evolved over the past decade².

What makes this particularly notable is that Texas has achieved this at a scale comparable with entire national electricity markets. The state now operates a renewable fleet that rivals or exceeds the size of some European countries. The pace of buildout has also been striking, with several years of rapid solar and storage growth that many markets around the world would struggle to replicate without heavy subsidy or a formal capacity mechanism.

The engine behind that growth has been different. Texas combines strong natural resources, relatively low land costs, nodal wholesale pricing, five-minute settlement, scarcity pricing signals, and investors willing to accept merchant exposure³.

That last point is crucial. Texas is not the UK. It does not rely on a traditional capacity market to provide guaranteed revenue floors for generation assets. ERCOT is fundamentally an energy-only market, where storage projects earn revenue through arbitrage, ancillary services, and scarcity events rather than fixed availability payments³.

OBBB accelerates the phase-down of several federal clean energy incentives and introduces stricter rules around supply chains and foreign entities. That matters because solar and wind projects now face tighter timelines and more complex procurement constraints. Early signs from the U.S. market suggest that policy changes have already created some disruption in project pipelines⁴.

But Texas still has something many markets do not: raw demand.

ERCOT’s long-term planning outlook shows a dramatic increase in future electricity demand, driven largely by data centers, population growth, and industrial electrification. Large-load requests tied to computing infrastructure alone now represent a substantial portion of potential future demand⁵.

This is why OBBB is better described as a filter rather than a stop sign. The United States still needs huge volumes of new generation. Texas still has some of the strongest conditions in the country for deploying it.

The projects most exposed are not necessarily the clean ones. They are the marginal ones. Poor siting, fragile supply chains, weak offtake logic, or overly optimistic financing assumptions will struggle in a more disciplined market.

The more thought-provoking issue is that Texas may be introducing a different kind of constraint at exactly the moment it needs to stay nimble.

One of Texas’s greatest strengths has historically been speed. Compared with Europe and much of Asia, developers could look at Texas and see a place where projects could actually get built. That relative speed mattered just as much as the sunshine.

Now the state is layering in more governance to manage reliability concerns, forecasting challenges, and the surge in large-load demand. Legislative changes and new regulatory processes are giving the system more tools to plan for rapid growth in electricity consumption and interconnection requests⁶.

These changes are understandable. A grid facing explosive demand growth cannot run purely on optimism.

But they are still a form of friction.

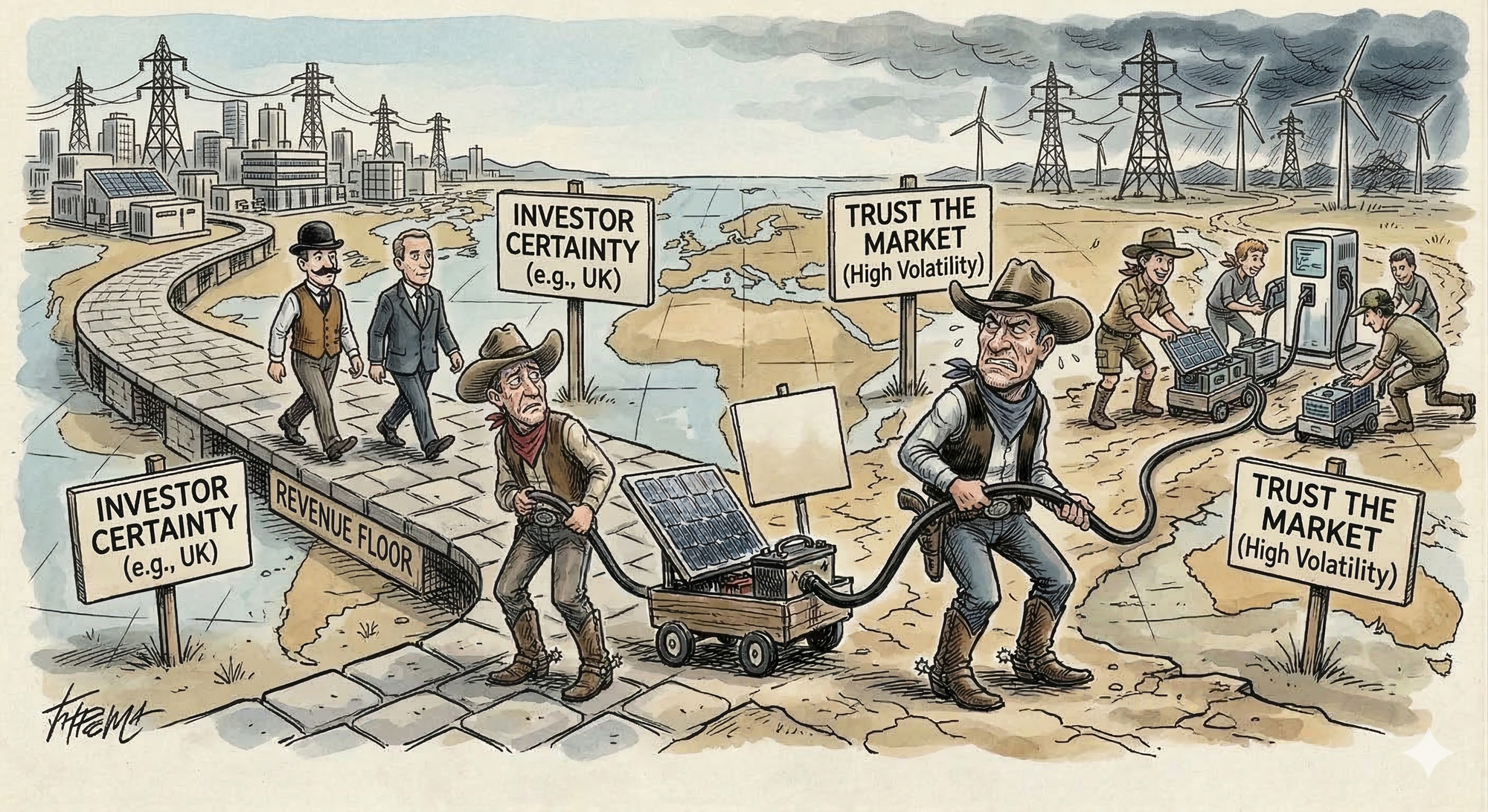

That is the balancing act. Texas became attractive because it was one of the few places where strong price signals and fast development timelines offset the risks of a merchant market. If the market keeps the risk but loses some of the speed, investors will inevitably begin comparing Texas more closely with other states and regions.

Not because Texas suddenly becomes unattractive, but because its advantage becomes narrower.

This is where the global comparison becomes particularly interesting.

On one hand, parts of the world are moving toward the Texas model. Electricity markets such as Australia have introduced shorter settlement intervals specifically to sharpen price signals for fast-response technologies like batteries and demand response⁷.

On the other hand, many international markets still provide greater investor certainty than Texas does. The UK uses a capacity market to provide a partial revenue floor for generators, while other regions rely more heavily on structured policy frameworks and market support mechanisms.

Texas still stands out for how much it asks investors to trust the market.

That works extremely well when speed and volatility are both in your favor. It works less cleanly when policy uncertainty and interconnection complexity begin to rise at the same time.

Another point that emerged during the panel discussion is that the next phase of the energy transition will not be defined purely by adding more generation.

It will be defined by how intelligently we operate the system.

ERCOT’s interconnection pipeline now contains hundreds of gigawatts of proposed solar and battery projects. Not all of these will ultimately be built, but the scale of the pipeline highlights the level of investor interest in the market⁸.

At the same time, distributed energy resources are becoming increasingly important. Residential batteries, electric vehicles, thermostats, and other flexible devices are beginning to play a meaningful role in balancing the grid.

Utilities and retailers are starting to aggregate these assets into virtual power plants, allowing thousands of small devices to behave as coordinated grid resources. Recent programs aggregating residential batteries provide an early glimpse of what this future may look like⁹.

Homes are increasingly becoming controllable grid assets.

In a world of tighter subsidies, rising demand, and more interconnection complexity, that matters. Utility-scale infrastructure provides bulk capacity. Distributed flexibility provides responsiveness.

The more friction introduced into building large infrastructure, the more valuable orchestration becomes.

Texas remains one of the most important clean energy markets in the country. But the rest of the United States is watching closely.

If Texas proves that an energy-only market can still deploy massive volumes of solar, storage, and flexible demand even as federal support declines, it strengthens the case for market-driven electricity systems.

If policy uncertainty increases, development timelines slow, and merchant economics become more difficult at the same time, other states may begin to look comparatively more attractive.

The future of clean energy in the United States will not be determined solely by subsidy levels. It will be shaped by speed, confidence, and market design.

Texas attracted enormous investment because it offered all three.

The question now is whether it can maintain enough of that advantage as the system grows more complex.

The old debate around clean energy was whether renewables could scale.

That debate is largely over.

The new debate is about which markets can continue to deploy infrastructure quickly once subsidies fade and system complexity increases.

Texas remains one of the best positioned places in the world to answer that question.

But it no longer gets to assume the answer will automatically be yes.

¹ ERCOT Seasonal Assessment of Resource Adequacy and grid resource reports

https://www.ercot.com/gridinfo/resource

² Houston Chronicle reporting on ERCOT solar generation surpassing coal

https://www.houstonchronicle.com/business/energy/article/texas-grid-solar-coal-21282343.php

³ ERCOT Market Design and Overview of the energy-only market

https://www.ercot.com/mktinfo

⁴ Reuters reporting on policy impacts on U.S. solar development

https://www.reuters.com/sustainability/climate-energy/us-solar-installations-down-2025-after-policy-changes-report-says-2026-03-10/

⁵ ERCOT Long-Term Load Forecast and large-load planning updates

https://www.ercot.com/files/docs/2025/04/07/8.1-Long-Term-Load-Forecast-Update-2025-2031-and-Methodology-Changes.pdf

⁶ Texas Legislature Senate Bill 6 legislation related to grid planning and large loads

https://legiscan.com/TX/text/SB6/id/3248460

⁷ Australian Energy Market Commission Five-Minute Settlement Reform

https://www.aemc.gov.au/rule-changes/five-minute-settlement

⁸ ERCOT Generation Interconnection Status and project pipeline reports

https://www.ercot.com/services/rq/generation

⁹ Vistra and Enphase residential battery aggregation program expansion

https://investor.vistracorp.com/2026-03-05-Vistra-Expands-Residential-Battery-Aggregation-Program-with-Enphase-Energy

Energy loves its acronyms, but it’s not always clear they’re helping. From HEMS to DERMS, this article explores how language meant to simplify can sometimes add to the confusion.

AI can write, plan, and predict but can it run the grid? This piece explores where it’s already adding value, where it still fails, and why the future of a “self-healing” grid will depend as much on people and infrastructure as on algorithms.

A drawer once full of tangled cables gave way to a single universal connector. The piece looks at how USB-C reduced friction, sped up charging, and what its success teaches about the value of standards, from consumer tech to home energy.